The financial world is replete with acronyms.

There are IRAs, ETFs, VATs, P&Ls, and hundreds of other terms to consider.

Today, however, we’re going to focus on two acronyms that every consumer needs to know:

APR and APY interest rates.

Though the terms sound similar (and are often used interchangeably), they’re quite different.

As you’ll see, it’s very important to know how APR and APY interest rates work.

The better you understand them, the more money you’ll save and earn.

What Is APR (Annual Percentage Rate)?

Annual Percentage Rate (APR) refers to the amount of interest you’ll pay each year to borrow money.

While APR is presented as an annual figure, most consumers make payments on a monthly basis (unless otherwise stipulated by the lender).

If you’re borrowing an installment loan, the APR will often include the interest rate along with accompanying fees (like the origination fee).

Conversely, if you’re obtaining a credit card, the APR generally won’t include any fees. Instead, it will simply show the interest rate you’ll be charged if you carry a revolving balance (i.e., if you don’t pay in full by the due date).

In most cases, the higher your credit score is, the lower your APR interest rates will be—improving your credit pays off.

Important: most credit cards often have multiple types of APRs, including Introductory APR, Cash Advance APR, and Balance Transfer APR. Be sure to carefully review the terms and conditions on your cardholder agreement to know exactly what rates you’re dealing with.

How To Calculate APR (And How It Works)

APR is calculated with this formula: Periodic Interest Rate x Number of Periods in a Year.

For example, let’s say ABC Bank offers a credit card with a monthly interest rate of 1.67%, just below the average interest rate in 2023.

In this case, the APR formula would be: 1.67% x 12 (months) = (approximately) 20% APR.

Now, let’s see that number in action.

Let’s say you purchased a $1,000 flatscreen TV using a credit card with a 20% APR.

Therefore, your account balance would be $1,000.

Next, multiply that number by the interest rate: 1,000 x 0.20 = $200. That’s the interest you’ll be charged over the course of a year.

Then, if we divide that number by 12, we see that you’ll pay roughly $16.66 a month during that year.

Keep in mind, if you don’t pay off the flatscreen TV in full, you’ll be subject to compound

interest. In other words, you’ll be paying interest on top of the interest you already accrued, all of which will be added to your original balance.

Most credit card issuers charge compound interest on a daily basis.

That’s how credit card balances get out of control. And that’s why it’s very important to always pay your balance, in full and on time.

To make sure you get the numbers right, we suggest using an APR calculator.

What Is APY (Annual Percentage Yield)?

While APR describes the interest paid on credit products, APY refers to interest earned on savings over the course of a year.

In other words, APR refers to what you pay the lender, while APY refers to what you get paid from the bank.

Though it’s not often presented in this way, any money stored in a savings account is technically a loan that you’ve given to that particular financial institution.

Here’s another important distinction to keep in mind: while APR (when paid on time) does not take compound interest into account, APY does.

While compound interest is dangerous on a credit card or loan, it’s very beneficial on a savings account, certificate of deposit (CD), or money market account.

After all, the faster interest compounds, the faster your savings will grow.

Note: we don’t mean to add another acronym to the already long list, but this is important to mention. In the financial world, APY is often referred to as the Earned Annual Rate (EAR).

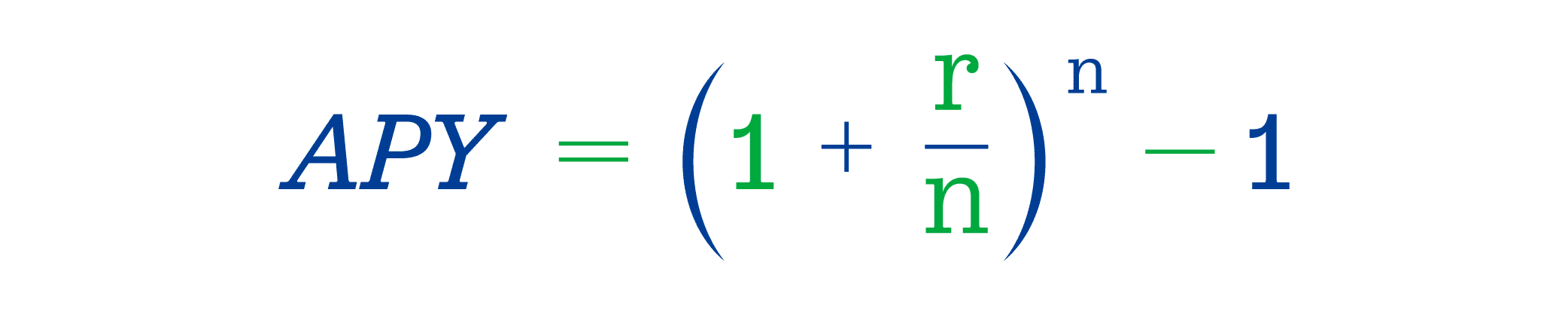

How To Calculate APY (And How It Works)

APY is calculated with this formula: APY = (1 + r/n )n – 1.

Here, the “r” represents the annual interest rate, while the “n” refers to the number of compounding periods each year.

If the interest is compounded monthly, for example, the “n” would be 12.

Let’s say you have an interest rate of 3% on a money market account where your interest is compounded monthly.

In that case, you’d use the aforementioned formula to calculate the following: APY = (1 + 0.03/12)12 – 1.

The result? An APY of 3.04%.

Remember, the APY formula always incorporates compounding interest. And as we’ve discussed, compounding interest is your ally, so long as it takes place within the confines of a savings account.

Though you’re welcome to run the numbers yourself, we recommend using a compound interest calculator to expedite the process (and prevent any unnecessary headaches).

APR vs APY: Summary

Though the acronyms seem similar, APR and APY have fundamental differences:

- APR calculates the amount of interest you’ll pay when you borrow.

- APY calculates the amount of interest you’ll earn when you save.

Therefore, the lower your APR, the less interest you’ll pay when borrowing. The higher your APY, the more interest you’ll earn when saving.

As always, be sure to read the fine print on all credit products.

Want to learn more? Check out our Comprehensive Guide to the U.S. Credit System for more answers to your most pressing questions.

P.S. Whenever you open a credit card or take out a loan, be sure to pay the balance in full by the due date. If you can do that, you’ll be in a great position to consistently grow your wealth.

Moving Forward

At uLink, we’re fully dedicated to furthering your financial freedom.

While promoting financial literacy and awareness, we do everything in our power to offer industry-leading exchange rates and fees as low as $0.

Our goal is simple: we want to make it easier than ever for you to send money abroad to your loved ones, wherever they may be.

Miles from home—just moments away with uLink.